In most countries, cash payments’ share of total payments volume is declining. However, cash in circulation (CIC) remains stable or up slightly over the past five years.

Cash has been resilient to the growing array of alternatives, even though transactional use is diminishing. Globally, CIC has increased from 4% to 7% annually over the last five years, despite lawmakers’ support of non-cash transactions according to The World Payments Report 2019.

Cash in circulation has been consistently growing across countries. A study by the Federal Reserve Bank of San Francisco concluded that the growth of cash circulation had outpaced economic growth over the last decade in 40 of 42 major economies in Europe, Asia, North America, and Latin America.

The growing trend became especially noticeable in advanced economies at the start of the 2008 global financial crisis and is likely driven by store-of-value motives rather than payment needs.

The store-of-value parameter has ticked up due to better cash-handling infrastructure in places such as ATMs. Moreover, the lower interest rates regime also encourages holding cash.

In Europe, cash represents 79% of all POS transactions in volume and 54% in value. Singapore, considered to be a mature market in terms of digital payments infrastructure, has high CIC as six of 10 transactions are carried out by cash.

At the retail/individual level, cash seems to be still indispensable for minor transactions (involving food supplies and groceries), personal security as a back-up, and small charitable donations.

Cash is still the ultimate recourse for payment transactions, as illustrated by the fact that CIC is up significantly in several countries undergoing distress, such as Mozambique, Myanmar, and Ukraine.

Interestingly, countries with the highest non-cash transactions volume also continue to be highly dependent on cash.

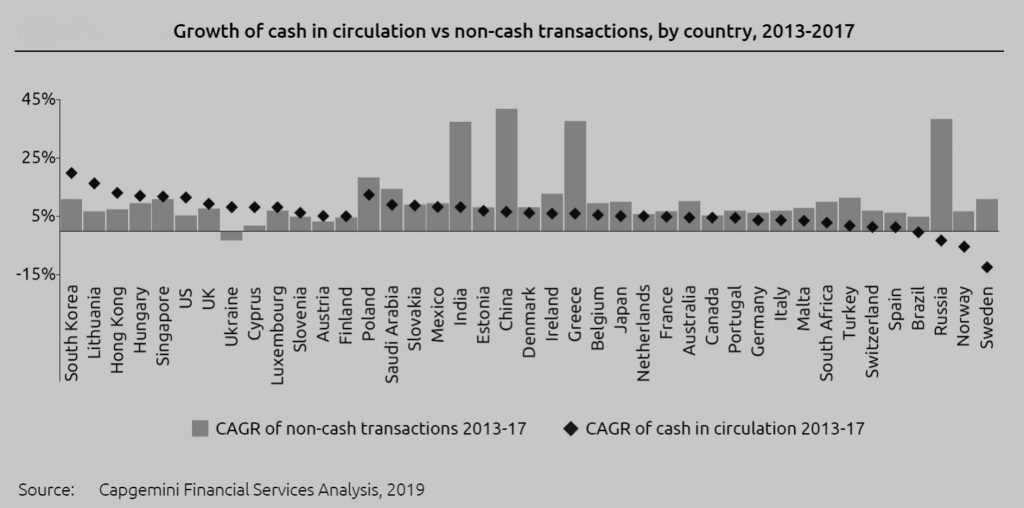

The unique set of needs that cash can fulfil makes a cashless world challenging to envision, although CIC continues to be affected by digital instruments. In the US, Finland, South Korea, Singapore, and the UK (with record- high non-cash transactions per inhabitant), CIC has grown steadily.

Even though these countries record high volumes of non-cash transactions, their economies support medium to high cash usage. Over 30% of the countries analysed in WPR 2019 recorded higher CIC growth when compared to that of non-cash transactions volume.

On the contrary, in certain countries, growth of digital payments contributed to decline in cash volumes. In Australia, digital payments soared 10% from 2016 to 2017, which led to a more than 5% decline in cash-usage during the same period. Singapore logged higher credit transfers as the government encouraged the use of PayNow, a common platform for conveniently making and receiving cashless payments across banks.

In Sweden, which is predicted to become the first cashless economy, non-cash transactions grew by 11% between 2013–2017 when the cash in circulation decreased by 12.4% over the same period.

In Russia, Poland, Lithuania, and Ireland, digital payments growth directly correlated to a growing cashless economy. Sweden is an exception to this trend as cash in circulation decreased by more than 12% from 2013–2017, while its non-cash transactions grew by 11% over the same period. However, cash is not totally out of the picture, as CIC grew by nearly 4% during 2016–2017.